The Bank Said No. We Have a Different Answer.

CapitalSource structures home equity solutions for borrowers conventional lenders can't qualify. If your income is complex, your documentation is non-traditional, or your profile doesn't fit a standard form this is where you start.

Secure intake · No obligation · No impact on credit

WHY CONVENTIONAL LENDERS KEEP SAYING NO

Most Lenders Are Built for W-2 Borrowers. Most Wealth Isn't.

Conventional underwriting was designed for one financial profile: a salaried employee with predictable pay stubs.

It was not designed for the self-employed entrepreneur, the real estate investor, the high-net-worth individual whose income lives in distributions and assets, or the homeowner whose equity is substantial but documentation is non-standard.

When those borrowers walk into a bank, the bank declines them not because of risk, but because of process. That is exactly the borrower we exist to serve.

Self-employed business owners and entrepreneurs

Real estate investors qualifying on property cash flow

High-net-worth individuals with asset-based financial profiles

Borrowers with complex, irregular, or non-traditional income

Aging homeowners seeking equity access without monthly payments

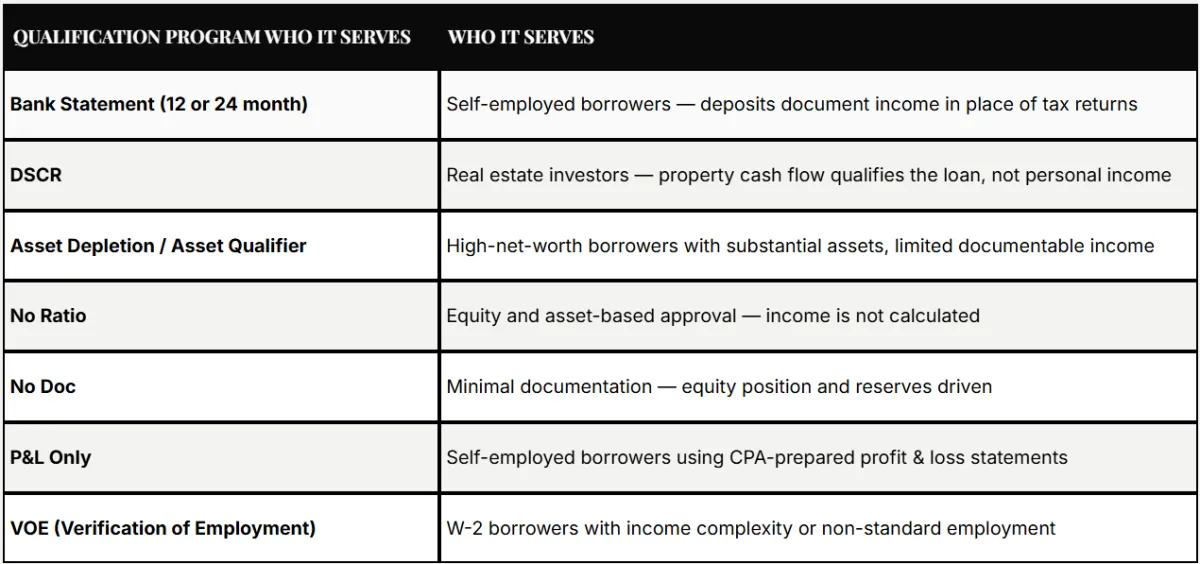

A DIFFERENT WAY TO QUALIFY

We Don't Start With the Tax Return. We Start With the Full Picture.

At CapitalSource, qualification is built around the borrower's actual financial position not a single documentation requirement. Depending on the structure, approval may rely on bank deposits, property cash flow, asset reserves, or equity position rather than traditional income verification.

QUALIFICATION PROGRAM WHO IT SERVES

WHO IT SERVES

Bank Statement (12 or 24 month)

Self-employed borrowers — deposits document income in place of tax returns

DSCR

Real estate investors — property cash flow qualifies the loan, not personal income

Asset Depletion / Asset Qualifier

High-net-worth borrowers with substantial assets, limited documentable income

No Ratio

Equity and asset-based approval — income is not calculated

No Doc

Minimal documentation — equity position and reserves driven

P&L Only

Self-employed borrowers using CPA-prepared profit & loss statements

VOE (Verification of Employment)

W-2 borrowers with income complexity or non-standard employment

COMPLIANCE: All loans subject to eligibility guidelines and credit approval.

A Focused Consumer Brand. A Complete Production Platform.

CapitalSource structures cash-out refinances across a full non-QM qualification stack. Approval can be based on bank deposits, property cash flow, asset reserves, or equity position.

Conventional, FHA, VA, Jumbo

Purchase transactions

Investor and DSCR products

HELOC, cash-out refinance, reverse mortgage

Full non-QM qualification stack across all loan types

Your clients see a focused specialist. You have the tools of a full-service platform.

HOW IT WORKS

A Structured Process. No Surprises.

1

Initial Review

We assess your property, equity position, and financial profile and identify which qualification program fits your situation.

2

Solution Design

We determine the right structure HELOC, cash-out refinance, or reverse mortgage and select the documentation path that gets your deal approved.

3

Execution

Clear terms. Defined expectations. Disciplined follow-through to close.

Ready to See What You Qualify For?

CapitalSource is a dba of EquitySource.

EquitySource operates as a mortgage broker and direct lender licensed by the California Department of Financial Protection and Innovation (License No. 60DBO-112262) and the California Department of Real Estate (Broker License No. 02111255).

NMLS ID 1936121.

© 2026 CapitalSource. All Rights Reserved.